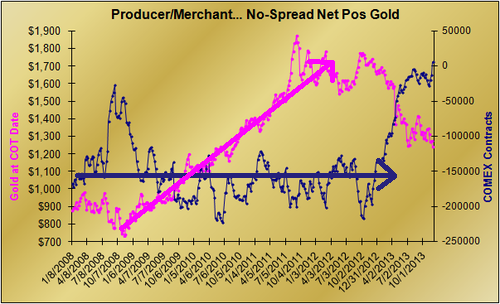

Gene Arensberg has a good post up on the rare occurrence of COMEX Producer/Merchants category going net long. He sees it as a bullish sign but I would suggest another interpretation which could be more ambivalent.

Gene notes that the producer/merchant "class of traders is dominated by actors who are hedging price risk of their own physical or financial exposure to precious metal, so they are usually more short than long futures" and that it includes "producers and miners, refiners, large jewelers, large bullion merchants". He also observes that for most of the time this group runs at around 160,000 contracts (circa 500 tonnes) short (see the chart below from Gene's site).

Now the interesting this about this is that this group stays pretty much consistently short right through a huge bull run in gold, in pink. Don't you think that is unusual? As the losses mounted, wouldn't they have lightened up? How to account for this behaviour logically?

The key is, as Gene says, that they are hedging their own physical. All of the types mentioned - miners, refiners, jewellers and bullion dealers - have a lot of gold in the working inventories of their businesses. They own this metal (are long) and thus go short to hedge themselves. Their business is about buying gold and transforming it into another more valuable product and then selling it. They are not interested in making money on the gold price itself.

Indeed, if they weren't hedged then as a group holding around 16 million ounces they would have lost around $11 billion dollars in the drop from $1900 to $1200. I'm pretty sure you'll agree that they are unlikely to be making so much profit making coins/jewellery or as coin dealers to wear that sort of loss.

So that is why we see a stable short position for this group, with smaller ups and downs as their sales and inventory fluctuate in response to changes in demand. If demand surges, then their inventory gets run down and they would take short hedges off and the short position would reduce. As they restock inventory, the short position should increase.

We now have a basis on which to explain the 2008/2009 and 2013 divergences from the long run average of 160,000 contracts short.

My explanation for the reduction in shorts from 160,000 to 27,000 in late 2008 is that the financial crisis caused an unprecedented surge in retail demand for gold. The industry was not geared up for that sort of volume so inventories were run down, resulting in a coin premiums surging. As the industry geared up and put on extra shifts etc the producer/merchants were able to restock and hence we see their short position increase again.

Continuing with this inventory based analysis, it suggests the interpretation for the 2013 reduction in short positions to 6,000 long is that the industry is running down its inventory. In 2008/09 the inventory run down was due to a demand surge, but was only temporary. In 2013 the run down has persisted. An explanation for that is that demand and business has dried up - if you aren't selling as much product then you don't need to hold, and can't justify holding, as much working inventory as you used to.

Consider that during 2006/2007 the producer/merchant short position hovered between 50,000 and 100,000 contracts (see this chart, which goes back a bit further than Gene's). The 160,000 average that Gene mentions is from 2009-2010-2011, which is the bull run in gold. An interpretation is that the extra demand during that bull run resulted in the industry needing to run higher inventories, so we see another 60,000+ shorts being added. With the $1900 bust, maybe the industry as a whole got stuck with higher than normal inventories so worked them down to their average of 75,000.

What is interesting is that the rapid reduction from 75,000 short to 6,000 long started after the April 2013 price smash. That event certainly knocked sentiment from the market in the West. It resulted in cash for gold scrap business drying up (therefore less metal tied up in inventories by dealers and scrap merchants) and if you look at US Mint gold coin sales, they drop right off from that point as well, so again coin dealers etc have reduced inventory needs.

To further back up this analysis, consider that US Mint silver coin sales have not reduced like gold and coincidentally the silver producer/merchant short silver position shows no reduction like gold as the silver market is still strong.

So I'd argue that the producer/merchant position is just reflecting the lack of Western interest in physical gold investment (as also demonstrated in gold ETF reductions) rather than them "believe[ing] the path of least resistance is higher for gold." Having said that, I wouldn't say it is necessarily bearish, as Gene is right in that it is a rare signal so could indicate a turning point. I just don't see it as a slam dunk bullish sign either, as this lack of interest in gold is likely to continue until people realise that, no, the economy isn't on the mend and the problems fixed. Until that mainstream narrative changes, we could see speculators testing the gold market to the downside.

Note: I have linked to a number of Nick's Sharelynx charts in this post. Just sign up for the free trial to get access to them, they are invaluable to understanding what is going on in the market, as hopefully this post demonstrates.

I forgot to include a note that my explanation is not meant as the sole reason as some of those entities in the group may also have spec positions as well, all going into the mix, I was just trying to say the inventory view is the base macro trend/driver for the short position.

ReplyDeleteInventory may be part of the explanation.

ReplyDeleteMy guess is that refineries historically have used hedges but have cut way back because the Chinese have been sucking up every available oz of gold so their speculative positions are way down. Perhaps the Chinese have given refineries open order to buy all gold at $1225 per oz changing their historical short position to long?

Miner inventories have actually been increasing modestly and they're not hedging. Jewellery consumption has been increasing. My guess is that gold jewellery inventory turns over 4 times per year. If true, gold inventory in stock is around 500 tons. Inventories could have been reduced significantly but I think they're still very significant resulting in the need to hedge.

Hi Bron,

ReplyDeleteI know that you would never give any investment advise, and that is good.

I am just wondering what is you own personal investment strategy when accumulating physical gold when saving for a long term (assuming that you buy physical yourself for that purpose?):

a.) Do you more try to time the dips or b.) buy more regardless of price on the regular basis?

When it comes to a.) or b.) do you have any own personal price limits when you say "that price right now is not sustainable concerning lower or upper limit", therefore I suspend or accelerate purchases?

Again, I am not asking for advestment advice just wondering about your own gut feeling.

Thanks&best greets, AD

Bron, I would like to know if the gold inventory needed for production at the Perth Mint has decreased substantially since April 2013.

ReplyDeleteETF reductions in physical doesn't fit this theory. There are 1000's of ETF's and most aren't for a physical commodity. Therefore the price can go up or down on paper and be arb'd without the need for creation or redemptions. The way I see it if physical gold is leaving an ETF that means someone wants to buy the gold. Wouldn't this indicate high demand for physical gold rather than low demand. In other words it makes more sense that the gold isn't pushed out by paper sellers but rather pulled out by physical buyers. This still won't be bullish for the price of gold in the short run....but in the long run, watch out.

ReplyDeleteyou're taking a bit of a verbal beating over at Turds World about your LME comment regarding Russ Winters latest article and the fact you or J.C.,KD or E.T.

ReplyDeletenever responded to his accusations.

the Mighty Turd might not realize you posted that "Apologist" post or that they actually responded to him or yourself there.

at this point the guy's ego has become a blindspot of self-confirmation bias. when a person won't (or can't) even consider anyone else's point of view because it upsets his comfort zone then what you have is an emotionally invested and compromised black/white static thinker who lacks sincere objectivity or real humility.

but hey, when you're a self-acknowledged salesman who admittedly is seeking to recoup $$$ from a failed past venture you'll relentlessly shill your product and say whatever your congregation wants to hear even if you know you're stringing people along like a cheerleader.

it's an interesting dynamic to watch over there. Trainwrecks are hard not to glance at when the conductor continues full speed ahead while the train derails.

ETF & COMEX are all rigged! So graphs and data like this is of no use!

ReplyDeleteWhat a load of nonsense. These blogger sites should be banned for the sophmoric comments that inexperienced rookies with a personal agenda just spew out without any fact basis.

ReplyDeleteNorm - if refiners are processing more 400oz bars into kilobars for China, then their inventories will be up. If they have a higher throughput they need a higher amount of work in progress stock.

ReplyDeleteAdvocatus, IMO you have to pay down debt as a priority. If you continue to run a mortgage (which in Australia is well above the official 2.5% rate), and are buying gold, then you are effectively buying gold on leverage. So I'm not buying gold. However, in Australia your employer has to put 9% into a pension plan for you, so as that is forced savings, then that is where you can do some allocation to gold if your fund allows it (I got our ASX listed PMGOLD product added to our company fund as an option). I think the permanent portfolio approach with regular rebalancing is a good option for your pension.

http://goldchat.blogspot.com.au/2013/10/gold-and-permanent-portfolio-in.html

Anon - our Depository and gold coin sides of the business have been slow. However, we don't run our inventory down as that is what backs client unallocated. Eg, if we owe 1000oz we have to have 1000oz in working inventory. If sales drop off then we just sit on the 1000oz. So we are bit different to business where inventory costs them money to fund.

ReplyDeleteSam - I don't think the ETF reductions have been about pulling out. Media reports have confirmed that a lot of institutional money has been flowing out of gold, so I think it is a case of pushing.

Anon - any link on TF where the chatter is? GATA posted on my response to TF so I assume TF readers follow GATA so would have seen it.

ReplyDelete"How to account for this behaviour logically?"

ReplyDeleteSince the highest quality good cannot be monetised, since it's already money, my analysis concludes that there is no logic.

It's also a much simpler explanation.

ReplyDelete"I don't think the ETF reductions have been about pulling out. Media reports have confirmed that a lot of institutional money has been flowing out of gold, so I think it is a case of pushing."

ReplyDeleteMoney flows through gold, not in and out of it. If physical gold moves there is a seller AND a BUYER, not just discouraged institutional money. Further as I said before ETF's have no obligation to reduce holdings of underlying physical when they are pressed by paper sellers, as evidenced by the 1000's of ETF's with no underlying physical assets at all.

Bron, it is an interesting theory, but does not explain why the American casino bankers have gone heavily long gold futures. Nor does it explain why JP Morgan furiously taking delivery of physical gold on COMEX for its HOUSE account! Historically, before every big drop in prices, per the COMEX bank participation report, American bankers go short. Similarly, they steadily build up long positions before a big price rise. These banks behave differently than the Euro-banks who also play the gold market, and whose positioning cannot be correlated with price movements. If we assume that their close connection to the Fed allows them to know, in advance, and front-run government subsidized price action, this becomes perfectly understandable. I cannot remember a time, ever in history, when the bankers were this long, nor do I remember a time when long buyers had a standing delivery request for almost almost the entire COMEX inventory (590,000 ounces compared to 700,000 ounces in total registered ounces). My personal suspicion is that JPM is being asked to repay loans stemming back for quite a long time, by the NY Fed's gold loan window. Remember, the White House calendar shows a meeting with all the CEOs of the 13 Federal Reserve primary dealers on April 11, 2013. Gold was smashed the next day, after pronouncements by GS suggesting that everyone get short on April 10th. We've seen huge unexplainable short sales within one second intervals, repeatedly, that have caused the CME's auto-stop trading software to kick in, and has overwhelmed the buy orders, taking down prices, at times by $10-30 per ounce within a few minutes. I believe that the entire operation, since April, has been designed to allow JPM to shake physical gold loose for purposes of repaying the Fed, so that the Fed could deliver gold to Germany, Netherlands and Switzerland, from a nearly empty vault underneath 33 Liberty Street, in lower Manhattan.

ReplyDeleteFor those curious about the meeting at the White House, where Obama himself, no doubt, authorized the subsidized gold smash that started on the 12th, see http://blogs.wsj.com/washwire/2013/04/11/full-list-of-bankers-at-white-house-meeting-thursday/

ReplyDelete"In 2013 the run down has persisted. An explanation for that is that demand and business has dried up - if you aren't selling as much product then you don't need to hold, and can't justify holding, as much working inventory as you used to."

ReplyDeleteThis part I don't understand. From the producers' perspective, if demand has dried up, the inventory should be up, not down, because demand normally drops much faster than production. Only when the producers manage to close down their mines will the inventory then drop but this usually takes a long time.

To follow up on my previous comment - what the blogger said may be true for a dealer if he can easily reduce its inventory. But his reduced inventory will result in inventory accumulating in the producer. So for the entire group of producers/merchants, if demand has dried up, the inventory should be up not down.

ReplyDeleteRCs comment seems logical to me. Inventory in this group dries up = lower demand for hedging = demand for physical is higher then actual supply . Low inventory (supply is tide) + actual price (attracting enough buyers) = long therm bullish for gold.

ReplyDeleteBron am I missing something?

Short therm gold price can go lower because of high speculative side short position. These are professional traders with deep pockets and sentiment is on their side (negative) thus I do not expect that they will loose money on this bet.

"physical gold moves there is a seller AND a BUYER"

ReplyDeleteyep, but both of those side are not necessarily on Comex or in the producer/merchant category, whose behaviour I was explaining.

in any case, if the buyer is Asian market, then the physical flow, particularly as the gold ETFs are physically backed and are not non-physical underlying ETFs as you claim - I'm looking here at GLD and the other key gold ETFs, not the 1000s of other ETFs you mention

"reduced inventory will result in inventory accumulating in the producer"

ReplyDeleteYou're looking at gold like it is widgets. There are three main products the industry produces - 400oz bars, cast bars, minted bars/coins - ranked in terms of increasing fabrication.

As you add more value, you need more metal tied up in work in progress inventories - coins take longer to make than 400oz bars. So it is possible for demand to drop in bars and coins, resulting in working inventory reduction but refiners can continue to process producers output into 400oz bars so there is no build up.

FYI, producers do not stockpile gold, they sell it ASAP. Hence industry inventories are related to the type of product manufactured and are used to support the flow. Those businesses in the industry do not have the financial resources/funding to stockpile gold in anticipation of demand, apart from the bullion banks themselves.

"yep, but both of those side are not necessarily on Comex or in the producer/merchant category, whose behaviour I was explaining."

ReplyDeleteexcept you also said in your post:

"the producer/merchant position is just reflecting the lack of Western interest in physical gold investment (as also demonstrated in gold ETF reductions)"

I wasn't disagreeing with the main subject of your post, just the example you give comparing it to physical redemptions in GLD.

"i'm looking here at GLD and the other key gold ETFs, not the 1000s of other ETFs you mention"

and i'm mentioning the non-physically backed ETF's in hopes that it would help shed light on the fact that physically backed ETF's do not *need to reduce or add physical in order to arb the NAV. It can be (and only makes sense that would be) done with all paper.